Industria italiană de tehnologie pentru prelucrarea lemnului și producția de mobilier trece prin perioade “complicate”. Datele preliminare pentru anul 2024 arată impactul “incertitudinilor” care au afectat de mult timp eficacitatea reală a măsurilor “Industry 5.0”, alături de consecințele durabile ale invaziei rusești în Ucraina și ale conflictului Israel-Palestina, combinate cu stagnarea cauzată de cererea excepțională din anii precedenți.

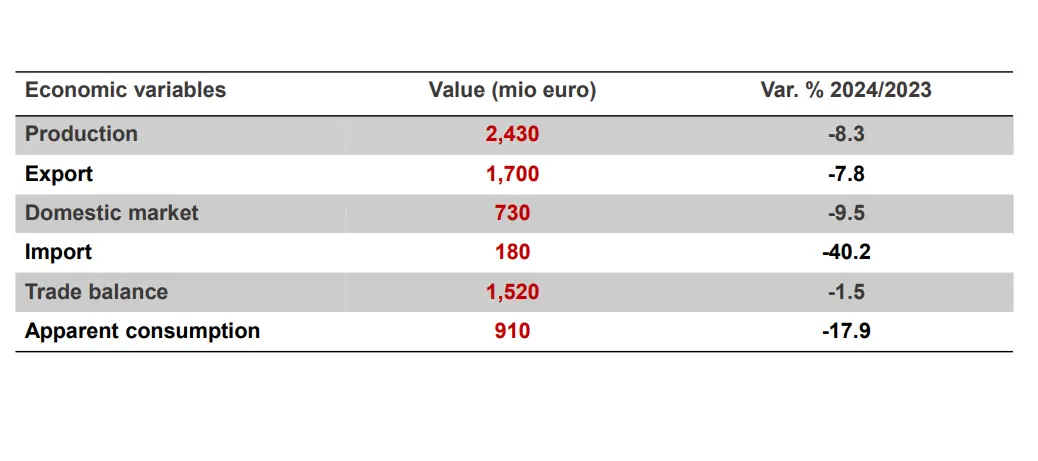

Conform bilanțului preliminar realizat de biroul de studii al Acimall, asociația membră Confindustria care reprezintă companiile din industrie, producția în 2024 s-a ridicat la 2,43 miliarde de euro, cu 8,3% mai puțin decât în 2023.

Această reducere a afectat atât exporturile (1,7 miliarde, scădere de 7,8%), cât și cererea internă (730 milioane, minus 9,5%), alături de o scădere accentuată a importurilor (180 milioane, minus 40,2%), demonstrând că oferta italiană poate “domina” cererea de tehnologie.

Această ultimă cifră a “susținut” de fapt balanța comercială (1,52 miliarde euro, în scădere cu 1,5% față de bilanțul final din 2023), în timp ce consumul aparent s-a oprit la 910 milioane, cu 17,9% mai puțin decât în anul precedent. Aceste cifre plasează Italia în primele poziții ale clasamentelor europene și globale privind cererea de tehnologie pentru lemn.

Situația pieței

“Situația nu este cu siguranță una pozitivă,” a declarat directorul Acimall, Dario Corbetta. “Industria suferă din cauza unei suspendări temporare a realității, mai întâi din cauza izbucnirii Covid, apoi a stimulentelor care au amânat problemele structurale ale industriei noastre timp de doi ani. Cauzele acestui scenariu sunt bine cunoscute: lipsa forței de muncă, schimbarea lentă între generații și toate provocările cu care se confruntă industria prelucrătoare mecanică, fără a uita tensiunile geopolitice care au împiedicat inevitabil exportul către unele piețe.”

Tendințe în export

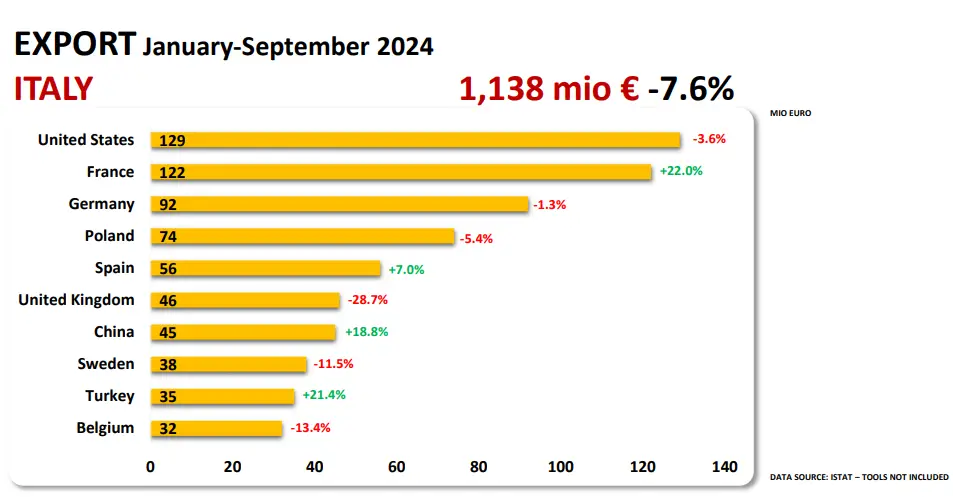

În primele nouă luni ale anului 2024, Statele Unite (129 milioane, minus 3,6% față de aceeași perioadă din 2023), Franța (122 milioane, plus 22%) și Germania (92 milioane, minus 1,3%) au ocupat primele poziții în clasamentul clienților Italiei, urmate de Polonia (74 milioane, minus 5,4%), Spania (56 milioane, plus 7%), Regatul Unit (46 milioane, minus 28,7%), China (45 milioane, plus 16,8%), Suedia (38 milioane, minus 11,5%), Turcia (35 milioane, plus 21,4%) și Belgia (32 milioane, minus 13,4%).

Evoluția exporturilor către China și Turcia este deosebit de interesantă, ambele țări înregistrând o creștere puternică a producției de utilaje pentru prelucrarea lemnului în ultimele decenii, devenind concurenți care trebuie urmăriți cu atenție.

“Faptul că producătorii italieni își pot consolida rolul pe aceste piețe nu doar demonstrează calitatea tehnologiei italiene, dar arată și că tehnologia avansată face diferența, deși pentru Turcia ar trebui să luăm în considerare posibile triangulații către alte destinații,” a adăugat directorul Corbetta.

Competitivitatea pe piețele globale

Italia continuă să joace un rol de lider în ceea ce privește competitivitatea pe piețele globale. În clasamentul țărilor exportatoare de tehnologie pentru lemn și mobilier în perioada ianuarie-septembrie 2024, China rămâne în frunte cu 1,827 miliarde euro export, cu 7,2% mai mult decât în aceeași perioadă din 2023. Locul al doilea este ocupat de Germania (1,807 miliarde, minus 12,4%), iar al treilea de Italia (1,138 miliarde, minus 7,6%).

Situația importurilor

La nivel global, Statele Unite au fost cel mai mare client pentru furnizorii globali, achiziționând mașini și instalații pentru lanțul de aprovizionare cu lemn din străinătate pentru o valoare totală de 1,782 miliarde euro, cu 0,8% mai puțin decât în primele nouă luni ale anului 2023. Pe locul doi, Germania (635 milioane de achiziții din străinătate, minus 8,2%), urmată de Canada (486 milioane, plus 8,4%).

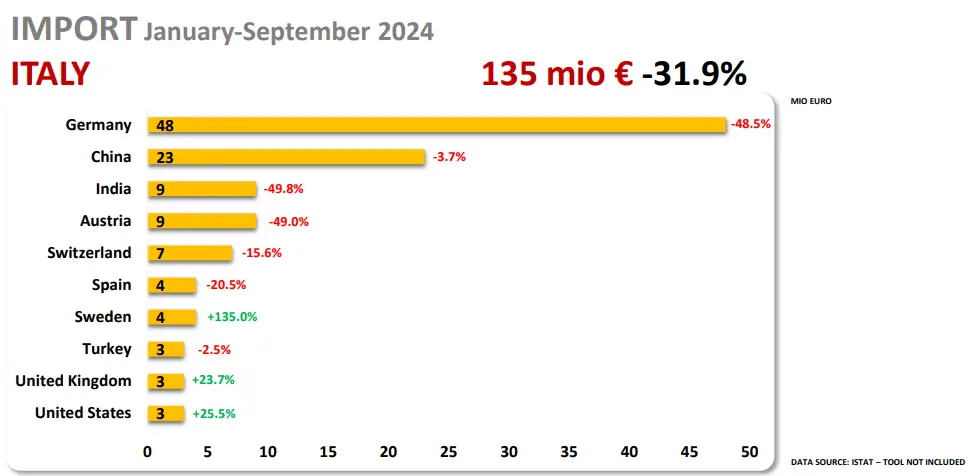

În ceea ce privește principalii furnizori ai Italiei în perioada ianuarie-septembrie 2024, primul loc în clasament a fost ocupat de Germania cu 48 milioane euro (minus 48,5%), urmată de China (23 milioane, minus 3,7%) și India (9 milioane, minus 49,8%).

Datele arată că, în ciuda dificultăților actuale, tehnologia italiană pentru prelucrarea lemnului continuă să fie apreciată la nivel global, în special pe piețe competitive precum China și Turcia.

Adaugă comentariul