Analysis of official statistics for the first half of the year shows an industry adapting to new global economic realities

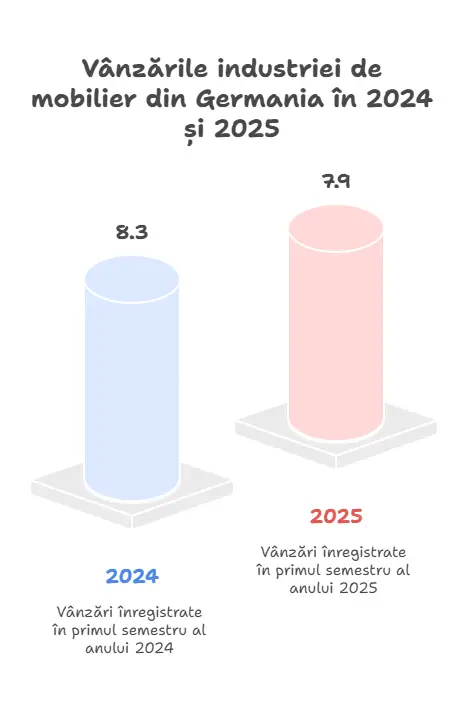

Germany's furniture industry, one of the most important in the world and a barometer for the entire European sector, recorded sales of €7.9bn in the first half of 2025, 5.1% less than in the same period last year. These figures, presented yesterday, August 26, 2025, at the German Furniture Industry Associations (VDM) annual press conference, reflect an industry facing complex challenges on multiple fronts.

Domestic market under pressure, exports holding up better

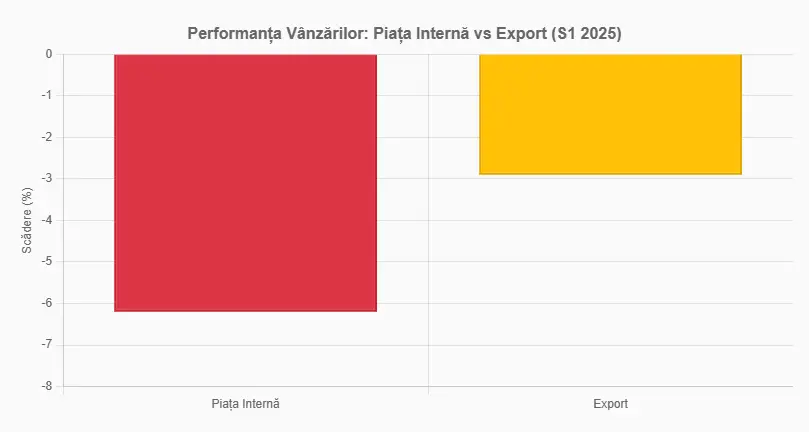

The differences between domestic and foreign market performance are significant. In the German market, sales fell by 6.2% to €5.2bn, while exports recorded a more moderate decline of 2.9% to €2.7bn. As a result, the export share increased slightly to 34.1%, compared to 33.4% in 2024.

Jan Kurth, executive director of the German Furniture Industry Associations (VDM), explained that "our industry continues to face difficult economic conditions: internationally due to the multiple effects of the US tariff policy, but especially on the domestic market".

Technical unemployment threatens one in three manufacturers

The difficult situation is also confirmed by companies' plans for the third quarter: 361TPTP3T of them plan to introduce technical unemployment, a measure that underlines the economic pressure facing the sector.

The companies' main concerns include the weak consumer climate and the downturn in housing construction. Although the new German federal government has proposed measures to simplify and speed up building permit procedures, Kurth believes that "without strengthening and increasing financing programs and additional measures to replace equity capital, the necessary momentum cannot be generated."

Excessive red tape becomes a growing burden

A growing problem for industry is excessive red tape, exemplified by the EU Deforestation Regulation (EUDR). Obligations to demonstrate deforestation-free supply chains mean a huge data transfer effort for industry.

According to a recent survey by the Main Association of the German Wood Industry, implementation costs for the EUDR can reach up to six-figure sums for furniture manufacturers, along with high running costs and additional staff effort.

Moderate recovery forecast for the second semester

For the fall, Kurth anticipates "a slight revival in furniture demand compared to the first half of the year". In Kurth's experience, after the holiday season is over, people turn their attention back to their own homes. "Rising real incomes will, in our view, help to realize deferred furniture purchases," he added.

The industry is also pinning its hopes on renovation needs. Against this backdrop, a decline of around 3% is forecast for the German furniture industry for the full year 2025, a decline that will not be as pronounced as in the previous year, when sales fell by 7.8% to €16.3bn.

Different performance by segment

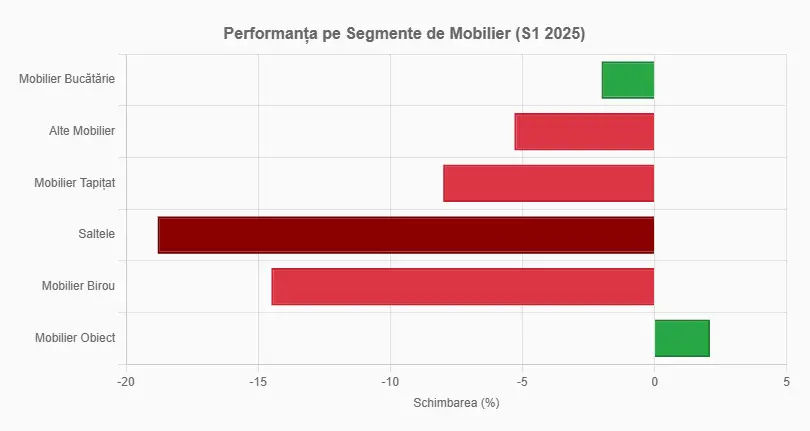

All consumer-oriented segments performed worse in the first six months compared to the same period last year, with dramatic differences between sectors, as can be seen in the segment performance chart.

The kitchen furniture segment proved the most stable, with a decrease of only 2% to almost €2.9 billion, where there was also a stabilization in orders. The "other furniture" segment (including living, dining and bedroom furniture, as well as furniture parts) realized sales of €2.4bn, a decrease of 5.3% year-on-year.

The situation becomes more dramatic in the other segments: sales of upholstered furniture manufacturers fell by 8% to €467 million, while the smallest segment of the industry - the mattress industry - saw a devastating drop of 18.8% to €217 million.

The impact of US tariffs on global trade

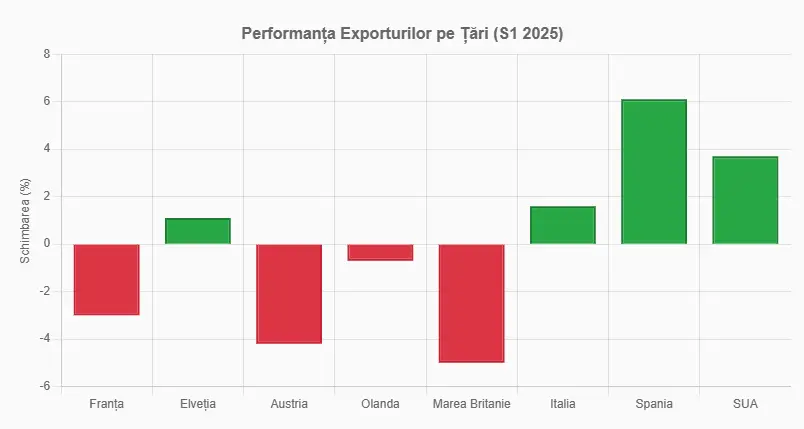

German furniture exports show considerable differences in the main markets, as illustrated in the chart on export performance by country. Sales to France, the largest export market, were 3% below the previous year. Furniture deliveries to Austria (-4.2%), the Netherlands (-0.7%) and the United Kingdom (-5%) also fell.

By contrast, Switzerland managed an increase of 1.1%, while exports to Italy rose by 1.6%. Particularly encouraging is the strong growth in exports to Spain of 6.1%, mainly due to the country's booming housing construction.

The United States is the most important non-European market for "Made in Germany" furniture, where sales rose by 3.7% in the first half of the year to around €132 million. However, the outlook is uncertain: most companies expect negative effects from the 15% US tariffs, according to a recent survey. 851TPTP3T of furniture manufacturers active in the US are bracing for declines in exports to the US.

Trade war cascade effects

In exports to China, the world's largest furniture market, German manufacturers suffered considerable losses (-42%). The reason is intensified competition on the Chinese market, after high US tariffs on Chinese furniture made Chinese manufacturers look for more opportunities on the domestic market.

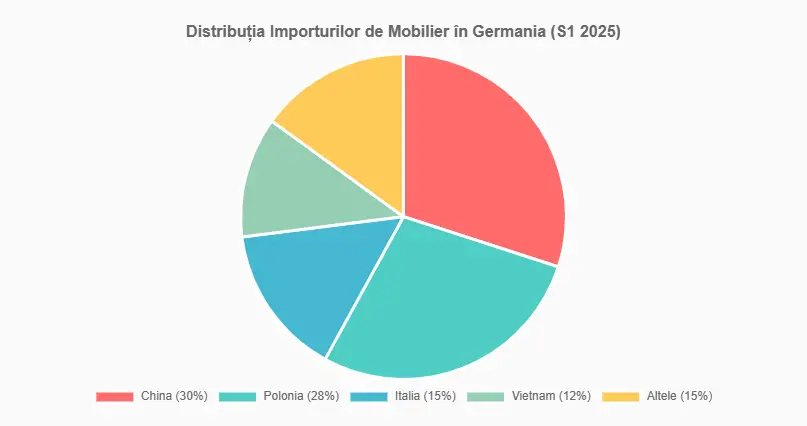

The effects of the US tariff policy are also being felt in furniture imports to Germany: due to the difficulties for Chinese furniture to be sold on the US market because of tariffs, more and more furniture from China is heading for the German market. The import distribution graph highlights this dramatic reality: in the first half of the year, furniture imports from China increased by some 25% to €1.7 billion, with China now accounting for 30% of German furniture imports.

The second most important supplying country is Poland with a share of 28%. Imports from Poland increased by almost 9% to almost €1.6 billion. Supplies of furniture from Italy (+27%) and Vietnam (+21%) also increased significantly.

In total, furniture imports into Germany increased by almost 15% to €5.6 billion. The most worrying aspect, clearly illustrated in the import share development graph, is that the import share of the German furniture market jumped dramatically from 53.1% in 2024 to 59.8% in the first half of 2025 - an increase of almost 7 percentage points in a single year.

Prospects for a changing industry

The German furniture industry, with 400 companies (with 50 and more employees) and a total of around 69,000 employees, is at a moment of strategic redefinition. Current challenges - from the difficult economic climate to changes in international trade and increasing bureaucratic pressure - demand adaptation and innovation.

Hopes for recovery rest on the recovery of domestic demand as the economy stabilizes and the ability to navigate the complexities of new international trade rules. For an industry with a long tradition of quality and innovation, these challenges may ultimately become opportunities to strengthen its position in the global marketplace.

Article based on official data presented at the annual press conference of the German Furniture Industry Associations, Cologne, August 26, 2025

Add comment